Risks and Rewards

Our journey into the investing world continues, and today we're tackling the fundamentals of risks and rewards. These are two fundamental elements that can make your investments grow or shrink, shaping your financial journey.

Understanding Risk 🚦

In investing, risk is the chance that you will lose some or all of your investment. For example, if you invest in a company’s stock, there’s a risk that the company might not do well, and the stock’s value could decrease. Risk, then, is the shadow of uncertainty that can affect your expected profits.

Some of the most common types of risks to consider include:

Market risk

Market risk means that changes in the whole market can lower the value of specific investments like stocks, bonds, and mutual funds. These changes can come from things like economic news, political events, or big global issues.

It's important to watch out for big global changes and events to understand this risk. Even if big drops in value don't happen often, they show how powerful market risk can be.

Credit risk

Credit risk is the risk to bondholders when a debt security issuer fails to pay interest or principal obligations in time. For instance, let’s say you invest in bonds from Apple, and suddenly it faces financial turbulence due to low iPhone sales during the year. As a result, the company may be unable to pay back its investors, and you stand to lose both income and potentially the entire investment's value.

To safeguard against this risk, it's important to research the financial health and credibility of bond issuers and diversify your portfolio.

Interest rate risk

Interest rate risk is the danger that bond values and other investments tied to interest will shift when interest rates change. For example, if you buy a 10-year government bond at a 2% interest rate and rates jump to 3%, your bond's value might drop because newer bonds paying higher rates become more appealing to buyers.

To deal with this risk, spread out your bond investments over varying time frames and keep an eye on factors that hint at rate changes, like central bank actions or economic signs.

Inflation risk

Inflation risk is when the real value of your investments might not keep pace with inflation and therefore reduce your money's buying power. This is especially true for fixed returns like from bonds, which might not grow as fast as inflation. Think of it like this: if you put money in a savings account with a 1.5% interest, but inflation is 2%, your purchasing power will actually decrease by 0.5% every year.

While cases of extreme and uncontrolled inflation are rare in places like the UK and Europe, it shows why it's vital to pick investments, like stocks or property, that can potentially grow faster than inflation.

Liquidity risk

Liquidity risk is when you can't easily sell an investment at a reasonable price. Investments that are not actively traded in an organised exchange, like certain small stocks, private businesses, or property, have higher liquidity risk. For example, if you own a valuable rare coin collection and suddenly need money, you might have a hard time quickly finding someone to buy it at the right price.

To handle this risk, it's good to have a mix of easily sold (liquid) and harder-to-sell (illiquid) investments and also some cash savings for emergencies.

Of course, this is not a comprehensive list of all possible risks. Each investment has its own unique characteristics and risks associated with it. Before investing, you should try to identify all relevant risks and quantify their impact.

Understanding Reward 🎁

On the brighter side of things, we have the reward. This is the profit you gain from your investments. When the company you've invested in performs well, the value of your shares rises. This increase, when you sell the shares, turns into your reward - the profitable outcome that keeps investors aiming for more.

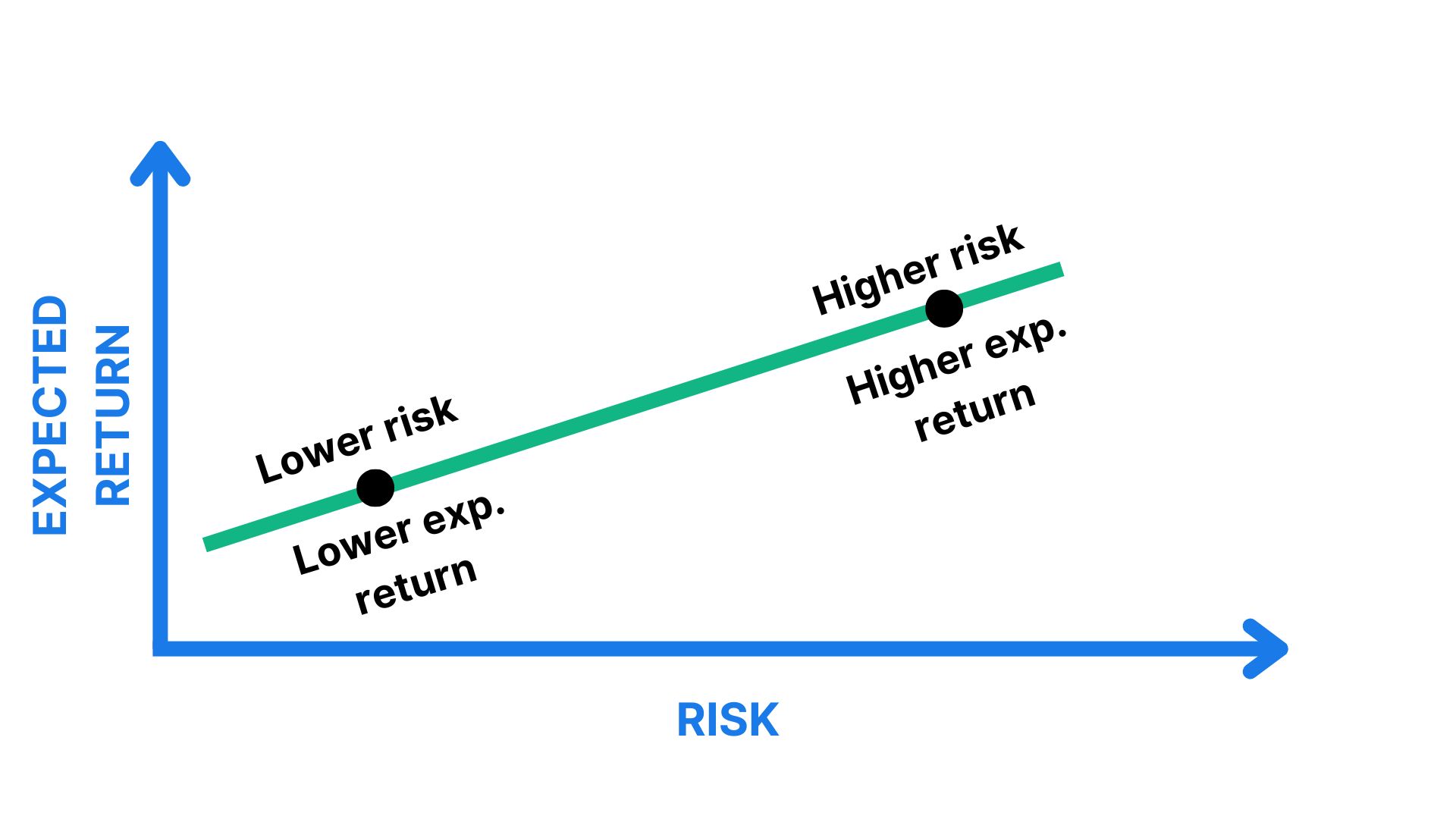

Risk 🆚 Reward

In the world of investing, higher potential rewards often come hand-in-hand with higher risks. For example, investing in a fresh, innovative startup could be a risk because new businesses can fail. But if that start-up blossoms into the next big thing, your reward could be huge.

Risk Appetite 🍔

Risk appetite is all about the level of risk you are willing to accept. Some people are thrill-seekers, ready to invest large sums in ventures like startups, despite the high risk, dreaming of substantial returns. They are said to have a high-risk appetite. Younger investors who are just starting out and who have more time to recover from potential losses often exhibit a higher risk appetite.

Risk Tolerance 🛡️

Risk tolerance, in contrast, is about how much risk you can afford to take. If you're near retirement, you probably can't afford to lose much. That means you have a low-risk tolerance. It's important to understand your risk tolerance, especially when you're investing to achieve specific goals, such as a comfortable retirement.

Appetite Vs Tolerance ⚖️

While risk appetite and risk tolerance might seem similar, they are distinctly different. You might be keen to take on high risks (showing a high-risk appetite), but if a loss would be hard for you to bear, you do not have a high-risk tolerance. Understanding both your risk appetite and tolerance can guide your investment decisions.

If, for example, your risk appetite is high, but your risk tolerance is low, you should manage this by creating a balanced investment portfolio to ensure that you don't overreach and put yourself in a difficult financial position.

Conclusion 🏁

The art of investing revolves around understanding and managing risks while chasing rewards. By being aware of your risk appetite and tolerance, you can tailor your investments to align with your comfort level and your financial goals. The secret lies in making well-informed decisions that align with your financial objectives.

We'll be diving into the world of traditional investments in our next lesson, giving you a closer look at some of the most common types of investments.