A

MyStudentFlat

EquityPropTechCIE Tax ReliefSeed

The first end-to-end Student Housing Platform in Cyprus, Greece and beyond.

€535,706

536% of minimum target96

Investors

Completed

The first end-to-end Student Housing Platform in Cyprus, Greece and beyond.

Investors

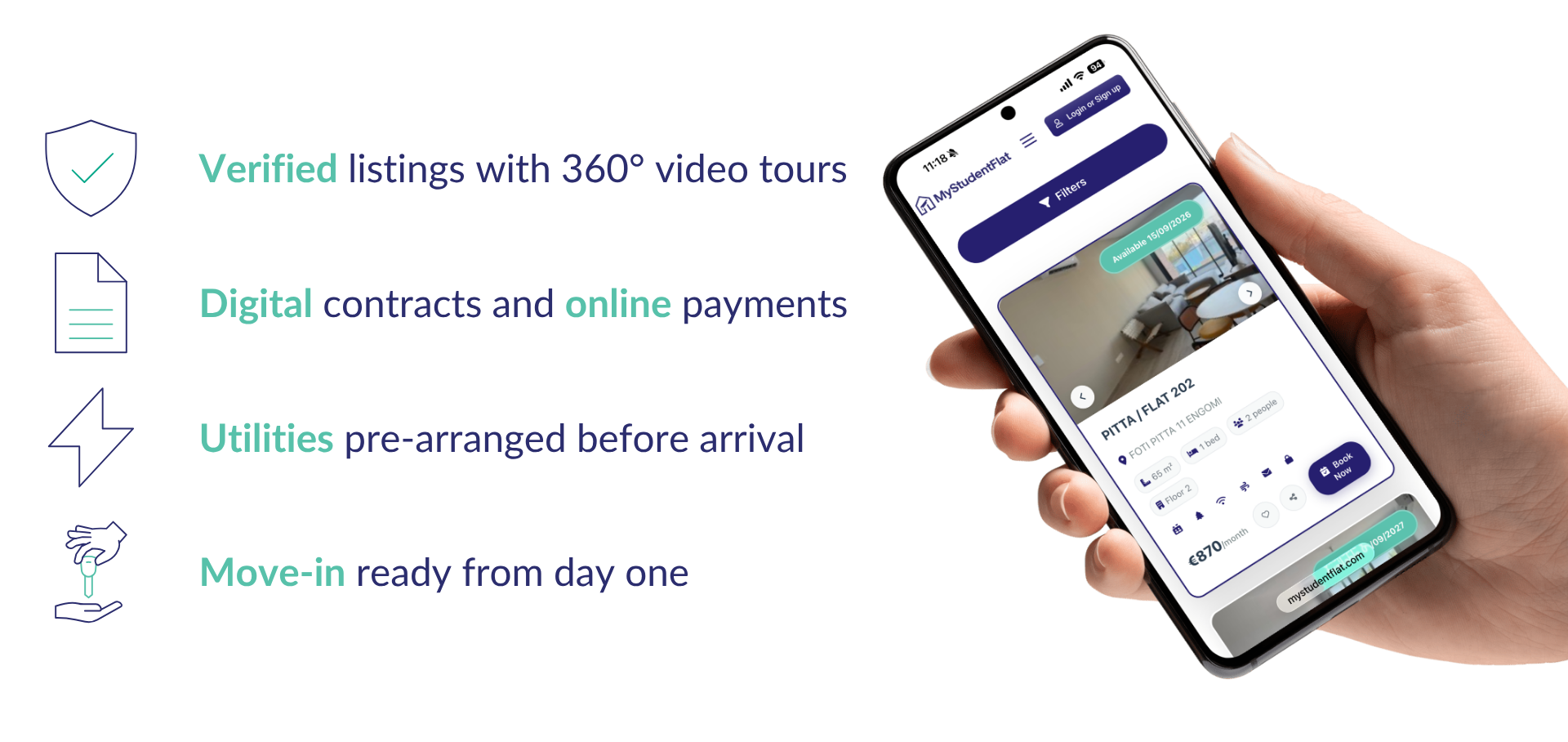

MyStudentFlat is the first end-to-end digital platform for student housing in Southern Europe. Already operating across Cyprus and Greece, we offer verified listings with 360° video tours, digital contracts, online payments, and pre-arranged utilities, so international students can book a flat from anywhere in the world and walk into a home that's ready on day one.

Cyprus and Greece host 800,000+ students with no dedicated digital platform serving them. The market is fragmented across classifieds, paper contracts, and individual landlord calls in a foreign language. The result is uncertainty and friction at exactly the wrong moment, as families commit thousands of euros to a flat they cannot inspect in person.

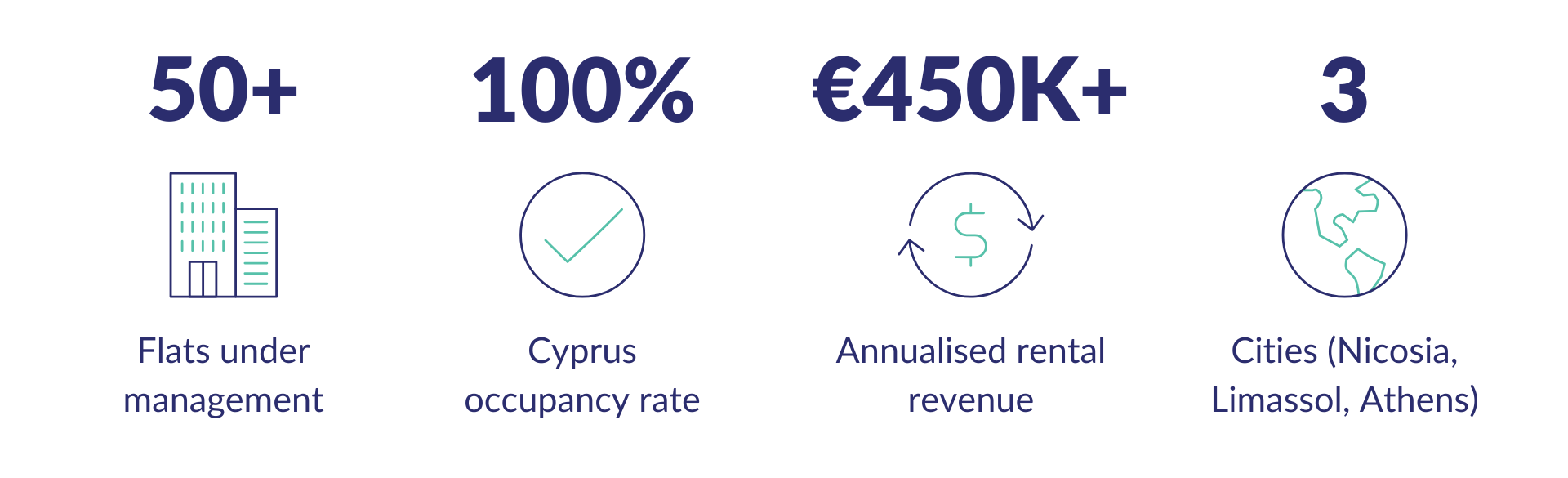

We launched commercial operations in September 2025. In the months since, we've grown to 50+ flats across Nicosia, Limassol, and Athens, with 100% occupancy in Nicosia and Limassol and more than €450K in annualised rental revenue. We have MoUs with European University Cyprus and the University of Nicosia, anchoring demand across our Nicosia and Athens markets.

We're now raising up to €500,000 to scale to around 200 units across both markets, complete the transition from operator to platform, and reach operational profitability in our first full academic year.

Picture a student arriving in a new country for studies at 23:30, suitcases in hand. They've spent months searching from abroad. They've called landlords who didn't pick up. They've made decisions based on photos that may or may not match the flat. They make their way to the address only to find the bed bare, the kettle missing, and the electricity not connected. The first night becomes a hotel room. The next morning, the bureaucracy starts: queueing in person at the Electricity Authority and the Water Board to transfer meters and pay deposits (€200 and €125 in Cyprus), hoping the line is short and someone behind the counter speaks English. Then linen, towels, kitchenware. All in a language they don't speak, in their first weeks of orientation.

For their parents, the anxiety is sharper. Financially committed, informationally blind, with no reliable way to know whether the flat their child is moving into is safe, clean, or even real.

This is the experience of millions of international students every year. The student rental market in Cyprus and Greece is fragmented, opaque, and built around in-person viewings, paper contracts, and word-of-mouth referrals. There is no standardisation, no verification, and no recourse when listings don't match reality.

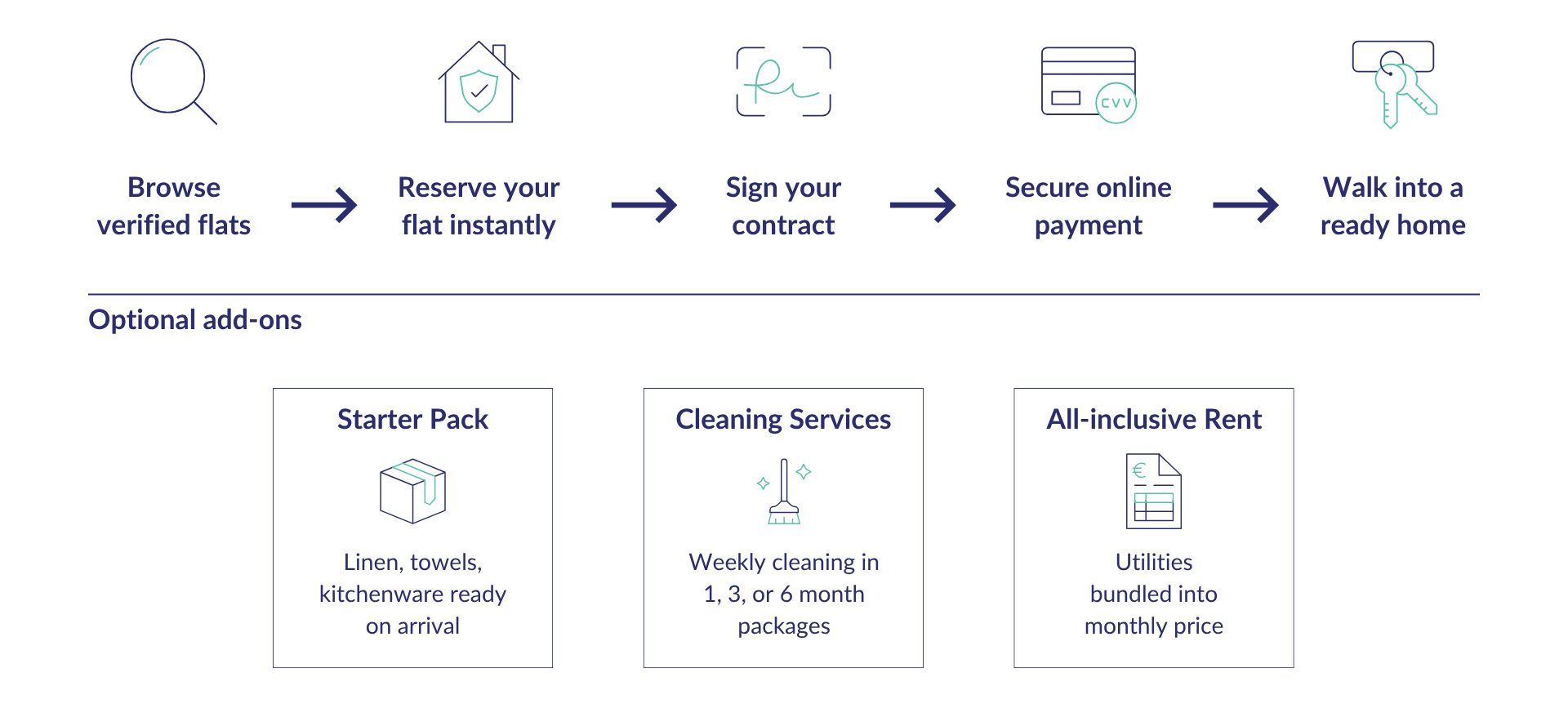

MyStudentFlat owns the full student accommodation lifecycle, from search to move-in. Students browse verified flats with high-quality photography and 360° video tours, reserve instantly, sign their tenancy digitally, and pay online. Before they arrive, electricity, water, and internet are pre-arranged. Optional starter packs (linen, towels, kitchenware) and weekly cleaning subscriptions are bookable in the same flow.

The result is a "Day 1 Ready" experience: a fully functional, verified, move-in-ready flat from the moment the student walks in. Done in minutes, not weeks. From anywhere in the world.

For landlords, the value proposition is just as clear. We deliver vetted tenants, professional management, on-time payments, and full operational handling of utilities, maintenance, and tenant relationships. All landlords we collaborate with prefer working with us instead of operating their properties in short-term rentals, because they get steady rental income and a partner who treats their flat with the same care as they do.

The full journey, end to end. No hassle, no paperwork, no past century bureaucracy.

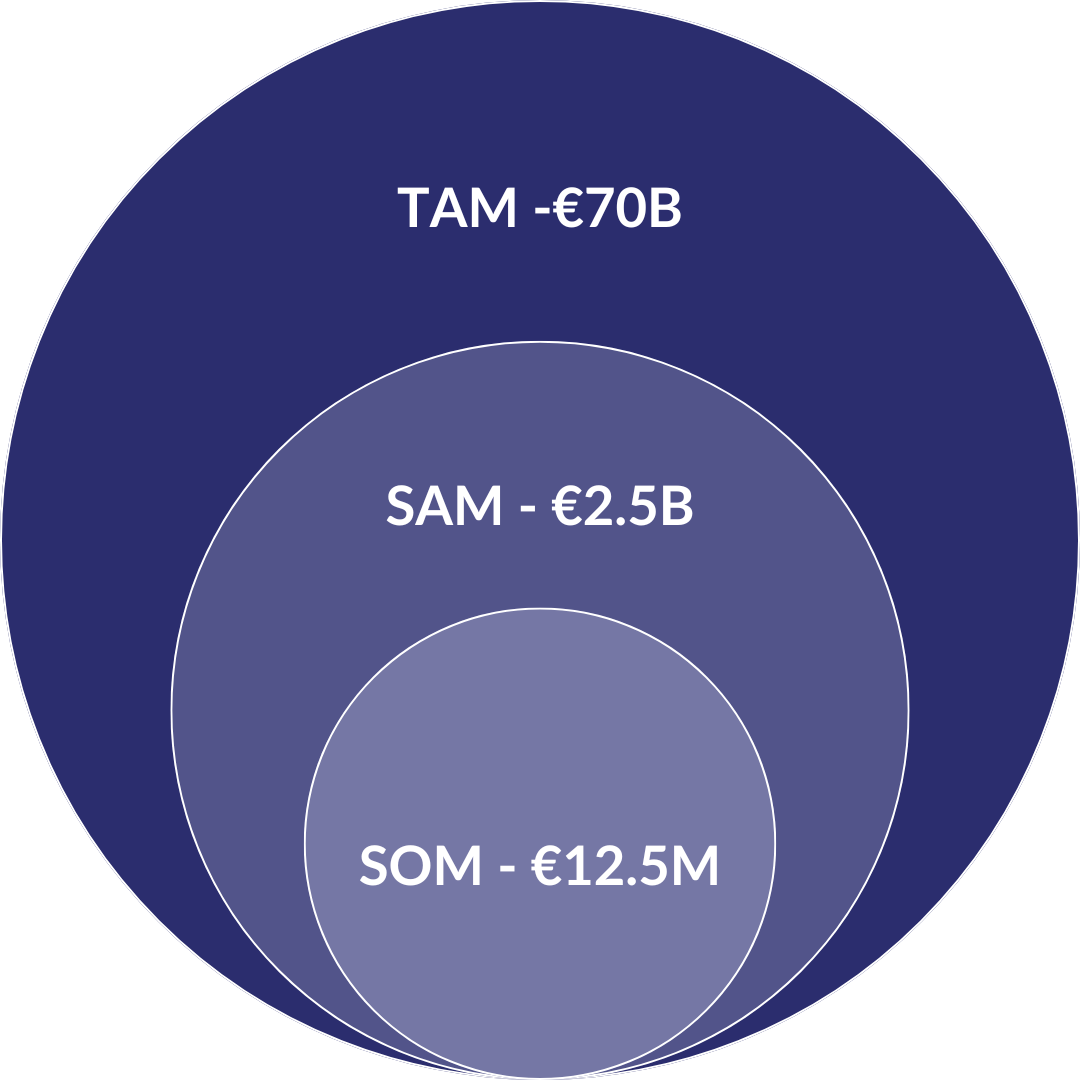

The European student accommodation market is worth approximately €70 billion and growing at 9.9% CAGR through 2031. Underpinning that growth is a structural 3 million bed shortage across the continent. New supply pipeline covers less than 5% of the gap, and average occupancy across major cities sits at 96%.

Within Europe, Cyprus and Greece are two of the most undersupplied and underserved markets. Cyprus enrolled 56,314 students in 2022-23, of which 56% are international and must secure accommodation remotely. Institutional student housing accounts for less than 5% of the market and is reserved almost exclusively for first-year students. From second year onwards, students are out in the open market with no platform-based option. Greece enrolled over 734,000 undergraduates the same year, with significant geographic dispersion driving domestic relocation, and zero platform-based competition for student housing. Together, the two markets represent a combined SAM of approximately €2.5 billion in annual rental value.

We target 0.5% of this SAM by Year 5, equivalent to roughly €12.5 million in gross rental value. That penetration leaves more than 99% of the market untouched, and is just a fraction of the market share that platforms like HousingAnywhere, Spotahome, and Uniplaces command in the Western European markets they entered first.

We operate three revenue streams, transitioning over time from operator to a fully managed student housing marketplace.

Today's primary stream. We sign long-term leases with landlords at wholesale rates and sublet to students at retail. Rental margins run around 17-20% per flat, varying by location, condition, and lease terms. Each tenancy also generates a one-off booking fee equal to half a month's rent at the time of booking. Assuming a conservative average tenancy of 2 years, this delivers reliable, recurring revenue per flat onboarded.

Our scale model. As we grow, we transition flats to a marketplace structure: landlords list directly, we collect a one-off commission and an annual management fee from the landlord, plus a booking fee from the tenant. The marketplace model generates lower revenue per flat but requires zero working capital tied up in landlord deposits, allowing the portfolio to scale far faster than the lease-sublease model alone would permit. All Limassol flats are already operating on this model at 100% occupancy, validating both the landlord and student value propositions ahead of broader rollout.

Starter packs, cleaning subscriptions, and all-inclusive utility bundles, all delivered through partner integrations. We earn around 20-30% commission on each. As tenancies grow, this layer compounds into a meaningful third revenue stream that strengthens the core proposition.

By August 2028 we target a 50/50 split between lease-sublease and marketplace flats, blending operator margin with platform capital efficiency.

Since commercial launch in September 2025:

University partnerships. The highest-leverage channel. We have MoUs with European University Cyprus and the University of Nicosia, anchoring demand across both Nicosia and Athens. Universities have a genuine gap to fill: on-campus housing is consistently oversubscribed, and most institutions only host first-year students. Students from second year onwards (including postgraduates) leaving university accommodation become a steady pipeline for us at the start of every academic year.

Digital marketing across booking cycles. Demand peaks around the August and January academic intakes, but bookings flow consistently throughout the year given the depth of the underserved market. We invest behind the peak windows with paid search targeting parents in Greece (the largest source of international students for Cyprus), SEO for university-specific keywords, and Instagram and TikTok collaborations with student creators.

Press and word-of-mouth. Press features in Greek and Cypriot media build brand recognition with parents during decision-making periods. Within the tight-knit Greek-Cypriot student community, satisfied tenants and parents are generating organic referrals that compound as the portfolio grows.

We sell to two audiences in parallel: students choose, but parents typically finance and decide. Our messaging is built for both.

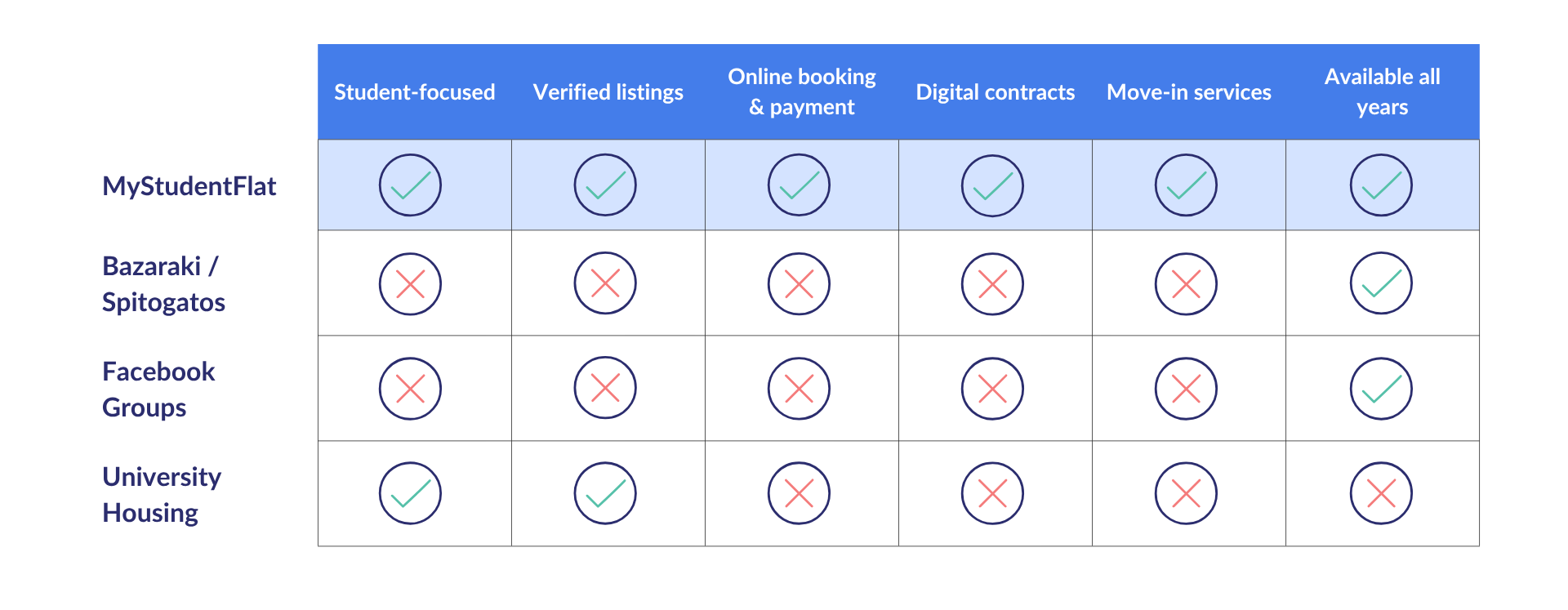

Students in our markets currently use Bazaraki, Spitogatos, Facebook groups, university off-campus offices, or general real estate agents. None of them solve the problem we do.

The European platforms (HousingAnywhere, Uniplaces, Spotahome) operate in higher-volume Western markets and have not entered Cyprus or Greece. These markets demand local relationships and operational depth that volume-optimised platforms don't typically build. The competitor we take most seriously is a well-capitalised local operator who could copy our model. By the time one launches, we will already have the landlord relationships, brand trust, and operational systems that take years to build, and a portfolio scale that is increasingly difficult to catch.

The European platforms (HousingAnywhere, Uniplaces, Spotahome) operate in higher-volume Western markets and have not entered Cyprus or Greece. These markets demand local relationships and operational depth that volume-optimised platforms don't typically build. The competitor we take most seriously is a well-capitalised local operator who could copy our model. By the time one launches, we will already have the landlord relationships, brand trust, and operational systems that take years to build, and a portfolio scale that is increasingly difficult to catch.

The market is not short on listings. It's short on a platform that takes ownership of the full lifecycle.

A trusted partner ecosystem already strengthens both sides of the marketplace. On the demand side, MoUs with European University Cyprus and the University of Nicosia anchor us across Nicosia and Athens. On services, Piney powers cleaning across both markets, TBI provides rental deposit financing for Greek tenants, and Proper Property runs credit control for our Cypriot tenants. Uniplaces, a leading European student housing platform, has partnered with us and cross-lists our flats to its international student audience, and Akoya Patrimoine is our French institutional partner for student-investor placements.

PropTech needs both by default. And MyStudentFlat team has both in its DNA.

Dimitris Economou, Co-Founder and CEO. Dimitris has spent over 15 years in student housing investing and real estate operations, personally building and managing a substantial portfolio of student flats around European University Cyprus and the University of Nicosia in Engomi. He brings hands-on knowledge of landlord economics, tenant expectations, and the operational realities of student accommodation. His Greek network runs as deep as his Cypriot one, which underpins our cross-border strategy.

Elena Orfanidou, Co-Founder, CTO, and CMO. Elena has built and scaled digital platforms in some of the most regulated industries in Europe. As Chief Digital Officer and Chief Experience Officer at Piraeus Bank, she led large-scale digital transformation. At Groupama Insurance, she served as CDO, Head of Innovation, and CMO. She also served as Chief Digital Officer and Board Member at Astrobank. Elena leads our technology stack and brand positioning.

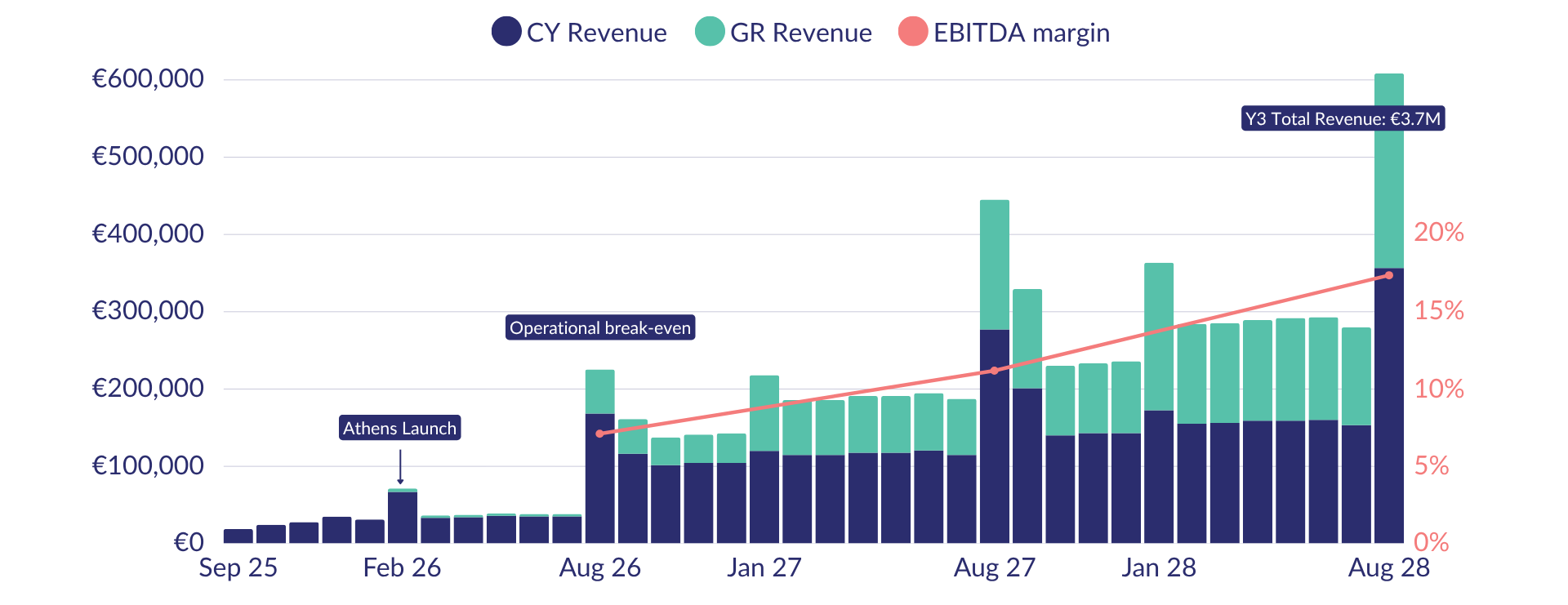

Our financial plan is built on a 36-month model with monthly granularity, beginning at commercial launch in September 2025.

Cyprus contributes the majority of revenue in Year 1. Greece scales to roughly half of total revenue by Year 3 as the Athens market matures and Thessaloniki and Patra enter the portfolio. The model mix transitions from 87% lease-sublease in Year 1 to 50/50 lease/marketplace in Year 3, lifting blended margins as we scale.

We expect to reach sustained monthly EBITDA profitability from December 2026, after our first full summer onboarding cycle has rolled through.

The model is favourably weighted on cash. Students typically pay rent annually or semi-annually in advance, while we pay landlords monthly or quarterly. The deepest cash demand falls in August, when summer onboarding deposits cluster ahead of student rent collection, and this raise is sized to bridge those cycles until the rolling portfolio funds itself.

Figures are illustrative projections based on current operations and contracted pipeline. Actual results may vary.

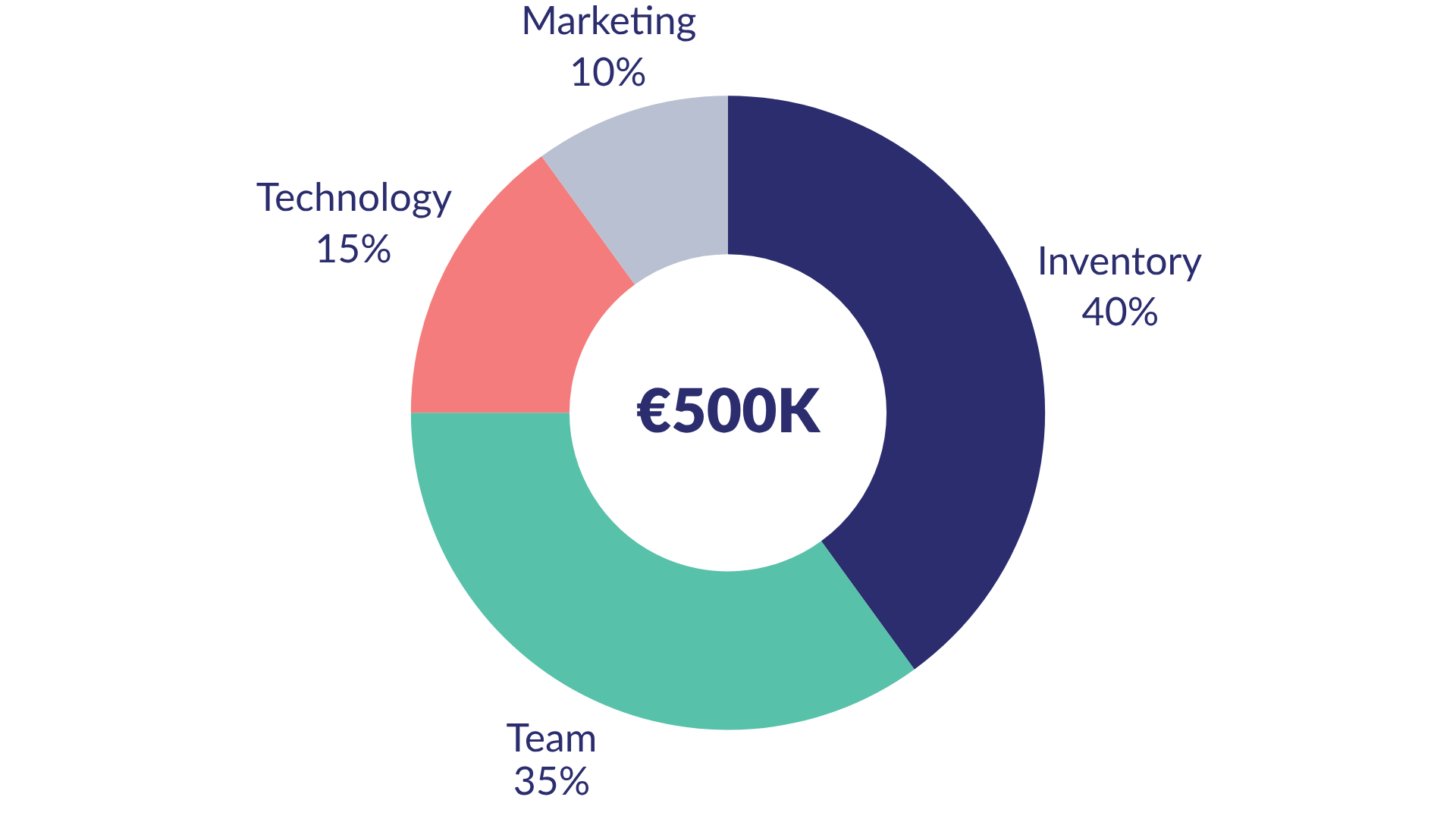

We're raising up to €500,000 in equity to fund the bridge from operator to platform.

40% to Inventory & Working Capital (~€200K). Landlord security deposits and utility transfers required to onboard around 150 new flats across both markets in the August 2026 cycle.

35% to Team (~€175K). Operations Managers in Cyprus and Greece, a Tech Lead to bring development in-house, and an in-house CFO to instil the working-capital discipline the lease-sublease model demands.

15% to Technology (~€75K). Cloud infrastructure, software subscriptions, and mobile application development. The core platform is already built and live.

10% to Marketing (~€50K). Digital customer acquisition and PR campaigns, timed to the August and January booking windows.

REPURPOSE TRAVEL & REALTY LTD has been certified as an Innovative SME under Cyprus's Innovative Enterprise scheme. Cyprus tax residents who qualify may be eligible for tax relief of up to 35% on qualifying investments in this campaign.

Investors should seek their own tax advice on eligibility and applicability.

While no one can predict the future, the European PropTech landscape gives us a clear set of potential liquidity paths.

Acquisition by a European PropTech consolidator. Platforms like HousingAnywhere, Uniplaces, and Spotahome have grown through both organic expansion and acquisition. As we build the leading position in Cyprus and Greece, we become the natural entry point for any of them into Southern Europe. The existing partnership with Uniplaces is a clear signal that big international players already consider us the serious local player in the student housing market.

Strategic acquisition by a real estate or hospitality group. Large operators in adjacent verticals (purpose-built student accommodation, hospitality, residential property management) are increasingly acquiring student-focused platforms to diversify their tenant base.

Profitability and dividend distribution. As EBITDA compounds and the portfolio scales, the Board may declare dividends to shareholders pro rata to shareholding.

Initial Public Offering. Over a longer horizon, as the platform matures and reaches the scale required to access public markets, an IPO on the Cypriot or Greek stock exchange may become a viable path for investor liquidity.

A future growth round may be required, possibly during 2028, to fund expansion into markets beyond Cyprus and Greece.

While timing and exact mechanism cannot be guaranteed, MyStudentFlat is being built with multiple paths to investor returns.